Future of Banknote Distribution in Australia

There is no longer any doubt that cash as a means of payment is declining – not just in relative but, increasingly, in absolute terms. The recent high demand for banknotes as a store of value only masks the reduction in their use for transactions.

There is also no doubt that cash performs a vital societal role and offers benefits that other forms of payment cannot. However, the fixed costs of cash are high – not so much in the volumes of notes and coins produced, but in the physical infrastructure for distribution. Steps to reduce these costs are leading to a vicious downward spiral, whereby reduced usage leads to reduced access which forces further reductions in usage, and so it goes on.

Central banks have traditionally been ‘neutral’ in the matter of payments. But in the case of cash, the market - if left to its own devices – will simply deal the final blow. Non-cash payment providers will see to that. Hence we are seeing an increasing number of central banks, and/or governments, stepping in – reviewing arrangements, launching consultations, bringing stakeholders together, even changing legislation.

The UK, the Netherlands and New Zealand are all examples of countries that in recent months have stepped up efforts to determine and define the future of cash in their countries. The latest to do so is the Reserve Bank of Australia (RBA), which this month published an Issue Paper as the start of a public consultation seeking views on how banknote distribution could be managed in the future.

Here we provide a summary of the paper since, although it aimed at those involved in banknote distribution in Australia, most countries sooner or later are likely to be considering the same issues; indeed, as above, some have already done so.

Changing cash usage

The use of cash in Australia is changing. Just as in many other countries, the value of currency in circulation is continuing to increase but physical cash is being used less as a means of payment. This trend has been accelerated by COVID-19 as consumers have moved more to electronic and online payments, and yet cash is expected to remain an important means of payment into the future, particularly by those who rely heavily on cash in their daily lives. Cash is also used as a store of wealth and as a back-up for electronic payments.

Currently the Australian public has good access to cash, the key elements of banknote distribution system having been in place since 2001 when cash was the most commonly used retail payment method.

But the declining use of cash for retail payments has led to lower processing volumes and underutilisation of the cash distribution infrastructure, thus increasing the cost of transporting and processing banknotes.

The RBA is concerned to create a banknote distribution system that enables good access to cash for the public but that is also sustainable. Its public consultation is designed to determine what changes are required so that banknote distribution is:

Effective – the distribution system enables demand for banknotes across the country to be met and supports the maintenance of good quality banknotes in circulation.

Efficient – the distribution system is cost-effective and enables the community’s cash needs to be met without prices being unreasonably high.

Sustainable – the distribution system is able to continue operating in the face of declining and/or comparatively low levels of transactional cash use.

Resilient – the distribution system is able to withstand disruptions and shocks to cash demand.

The cash landscape in Australia

Over the decade prior to COVID-19, banknotes in circulation grew by around 6% annually, outstripping GDP growth. But during the pandemic, demand has been extraordinarily high, with the value increasing by around 20% between February 2020 and October 2021 when it reached $100 billion, double the value in 2010.

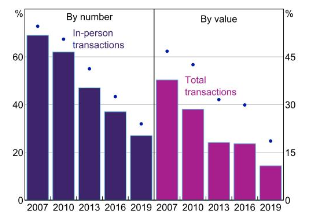

However, the RBA’s Consumer Payment Survey shows the share of total retail payments made with cash, both in-person and online, fell from 69% in 2007 to 27% in 2019.

Cash is used mostly used for low-value transactions, so as consumers have switched away from it, the demand for low value banknotes ($5, $10, $20) has declined.

Part of the acceleration of the decline in cash usage during the pandemic is expected to be temporary, but much is expected to be permanent. However, cash remains an important means of payment for some members of the community - the 2019 RBA survey indicated around 15% of people use cash for 80% or more of their in-person transactions (compared with around 45% in 2007) – ie. those who are older, on low incomes, who live in rural areas and/or with limited internet access. These people would suffer major inconvenience or genuine hardship if cash was not accessible.

As in Europe, North America and elsewhere, the increase in banknote circulation in Australia, despite declining transactional use, can be attributed to the growing role of cash as a store of value, as exemplified by the demand for high value banknotes – around 73% of the number and 94% of the value of banknotes in circulation are accounted for by the $50 and $100 denominations.

As a result, cash is circulating less, which has a significant effect on the cash distribution system and its participants.

For example, the value of ATM withdrawals has fallen by around 40% and the number of withdrawals by 66% since 2012, with similar declines for cash withdrawals from other sources.

Lodgements from retailers to cash institutions via commercial cash depots have also fallen significantly – both the number and value were around 55% lower in September 2021 compared with 2012. This trend has accelerated during the pandemic and, as with retail payments, it is unlikely that ATM withdrawals or cash depot lodgements will return to pre-pandemic levels.

Banknote distribution system

The issuance of banknotes is governed by a series of legal agreements, known as the Banknote Distribution Agreements (BDAs), between the RBA and the four major Australian commercial banks.

These agreements, which are periodically renegotiated, cover meeting demand for banknotes, including the wholesale banknote purchases and returns, as well as payment of interest compensation to BDA participants on their cash holdings. They also cover maintaining the quality standards for banknotes in circulation by accurately sorting to the standards specified by the RBA, for which the RBA pays.

Only BDA participants can purchase banknotes directly from the RBA. BDA participants are also encouraged to buy and sell surplus banknotes from one another. This is also how organisations that are not party to a BDA are able to obtain banknotes.

The distribution of banknotes throughout the country is carried out by the private sector. The BDA participants engage CIT companies to transport, process and store banknotes on their behalf. In order to collect banknotes from the RBA, these CIT companies must be nominated by a BDA participant and approved by the RBA.

These approved CITs collect banknotes from the RBA’s distribution site and transport them to their cash depots for distribution to bank branches, ATMs and retailers throughout Australia.

Banknotes are returned to the RBA by approved CITs on behalf of the BDA participants and ownership transfers to the RBA on their receipt when they are deemed to be out of circulation.

Over the last 10 years, $5.5 billion worth of banknotes (160 million) have been returned to the RBA each year on average, compared with $10 billion worth (240 million) that were issued by the RBA each year.

Two types of banknotes are returned - surplus and unfit. The former are stored and reissued into circulation as demanded, the latter processed by the RBA - counted, authenticity confirmed, unfit banknotes removed and destroyed, and fit notes repackaged and returned to circulation as demanded.

The Australian CIT industry

In the cash distribution system, the CIT companies are responsible for moving and processing banknotes. Their unit costs are increasing as transactional cash use declines, which is putting financial pressure on some parts of the industry.

There were more than 300 companies providing CIT services in Australia in 2015, with about 120 of these doing regular CIT work. However, there are two dominant players, Linfox Armaguard followed by Prosegur Australia, who together account for 70-90% of the market. Both conduct wholesale cash distribution as well as servicing the cash related needs of financial institutions, large retailers etc.

The main issues facing the CIT companies are 1) high fixed costs as well as a declining revenue base and 2) underutilisation due primarily to the decline in cash usage for retail payments.

Australia’s vast size and relatively low population density also contribute to the costs of meeting demand for cash services in remote locations. Combined, the result is a material effect on the profitability of some businesses and is particularly acute for the larger CIT companies.

One solution could be for these CIT companies to increase prices, but this may prompt businesses to use less cash or no longer accept cash, thereby reducing the public’s ability to use cash.

Also, should the profitability of one of the larger CIT companies fall beyond its business being economically viable, it could exit the market. Cash distribution, and with it access to cash, could be disrupted, at least in the short term.

Declining cash usage has also led to significantly lower processing volumes and in turn excess capacity at some CIT depots. This situation has worsened with a sharp decline since the start of the pandemic (from above 70% to below 60%); current estimates indicate that depot utilisation (based on banknote flows between cash depots and customers) may be as low as 50-65%, but is unlikely to be uniform across the country. RBA estimates suggest utilisation may be somewhat higher in major cities compared with regional areas.

The RBA estimates suggest that in 2020, Australia-wide cash demand could have been met by around 20-30% fewer depots than were in operation, suggesting there may be efficiency gains from a different business model, particularly if the decline in transactional cash continues.

Banks and CIT companies have made some changes in response to the decline in cash usage. Between 2017 and 2021, bank branch numbers fell by more than 20% and the number of ATMs by around 20% from its peak in late 2016, but the number per capita remains in line with other comparable countries. Current RBA estimates indicate that 95% of people live with 5 km of a cashpoint.

Recently several banks have sold parts, or all, of their off-branch ATM fleets to third party operators (generally CIT companies) and pay for their customers to access the machines on a fee-free basis. Such arrangements could be a more efficient way to sustain a broad coverage of ATMs, especially in regional and remote areas where there are fewer options for accessing cash services. The RBA has supported this development that enables card issuers to access other participants’ ATM fleets, thus providing cardholders with wider access to fee-free ATMs.

Another option for CIT companies to reduce costs is new technologies, such as smart safes which reduce the necessity for frequent cash-pickups, thereby allowing CIT companies to optimise transport costs. Another possibility is recycling ATMs, especially in remote parts of the country.

Options for cash distribution

The RBA in this section considers options that seek to, first, address excess capacity in the CIT industry and, second, identify considerations for the structural arrangements that underpin wholesale banknote distribution.

The RBA considers that the declining transactional use of cash is potentially leading to mounting excess capacity within the CIT sector. While in part due to COVID-19 and lockdowns, it considers it unlikely that transactional cash will recover to pre-pandemic levels and that the decline in cash use as a means of payment will continue.

It has identified various courses of action that could help address these issues. Any changes should be managed so as not to materially disrupt cash access across the country.

Three such courses are:

Existing participants work together to improve the efficiency and viability of their operations.

CIT firms coordinate to remove excess capacity.

Consolidation that results in one main entity being responsible for some or the majority of wholesale cash distribution.

It noted that consideration with respect to these options would be to ensure that there is continued good access to cash across the country and that competition issues that arise are appropriately managed. This may require additional policy responses, potentially including action by the RBA or government.

Suggested options for changes that improve the efficiency of the wholesale cash distribution arrangements include:

Changing the nature of public sector involvement.

Consideration of quality arrangements.

Segmenting the BDAs.

The options, the RBA points out in its final remarks, are not intended to be an exhaustive list and alternative suggestions are welcome. It also points out that most likely a series of changes to the distribution system are required rather than a single ‘quick fix’.

The RBA, which posed a series of questions in the paper, is now seeking views from interested parties on these questions, and inviting stakeholders to raise other issues relevant to the banknote distribution system that they would like be considered as part of this review.

Written submissions should be provided no later than 21 January 2022. A subsequent paper, which is expected to be released in mid-2022, will provide a summary of the consultation responses and set out recommendations.

In the meantime, the paper can be downloaded here.

Subscriber content

Read the full article

Full access to Currency News articles, newsletters and archives.