Good Results Fail to Impress the Markets

We end 2021 as we began it, with a new coronavirus impacting our health, freedoms, family and daily life, companies, jobs, economies and global trade.

The emergence of the highly infectious COVID-19 Omicron variant is a major blow to a return to relative normality, which appeared to be on the horizon for 2022. It is clear, as predicted by most virologists, that the fight to constrain COVID-19 is neither going to be easy nor short term.

Elsewhere in this month's issue of Currency News, there are articles covering the impact COVID-19 as well as digital payments on cash usage and the implications regarding the availability and role of cash in the future. While the companies we feature in Industry Watch are being directly affected by these trends and issues, they are also subject to market trends.

COVID-19 has disrupted global economic stability – raw materials, energy and labour are all in short supply, and inflation is on the rise. It has just reached 6.8% in the US, 6% in Germany and 5.1% in the UK. This is likely to lead to money tightening and rises in interest rates. These trends do not bode well for equity markets.

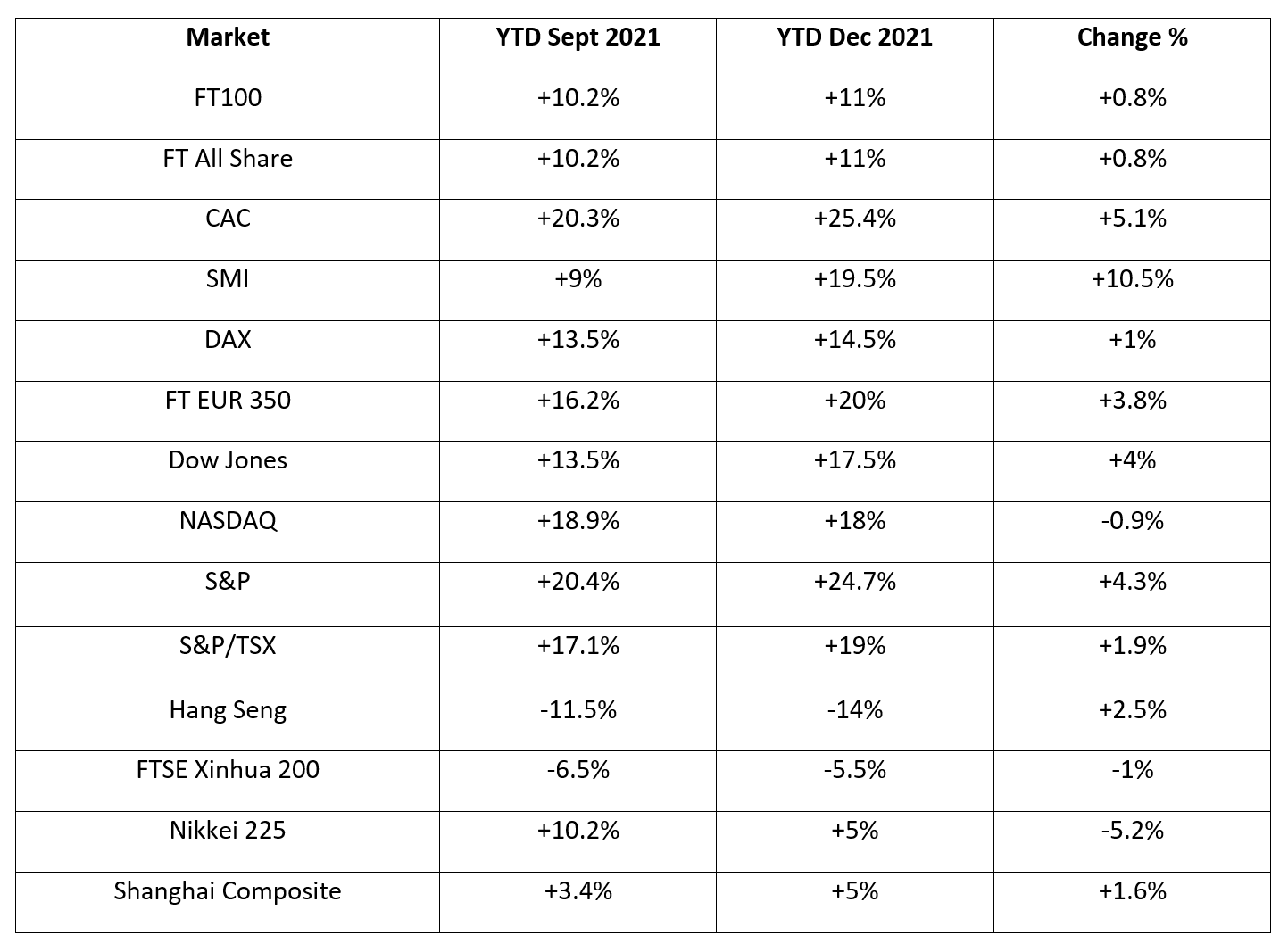

The performance year to date of the main markets in the countries in which the companies we follow is listed in Table 1. As can be seen, most European and Americas markets gained in the quarter. In Europe, the Swiss SMI rose by 10.5%, the French CAC by 5.1% and the FT Euro350 by 3.8%). In the US, the Dow Jones (+4%) and the S+P (+4.3%) were the standout performers, but in Asia only the Shanghai Composite gained (+1.6%).

Year to date the gains are substantial, with all markets in Europe and the Americas gaining between 11% and 25.4%. In Asia only two of the four markets recorded gains – the Nikkei and Shanghai Composite both gaining 5% with the Hang Seng losing 14% and the FTSE Xinhua 5.5%.

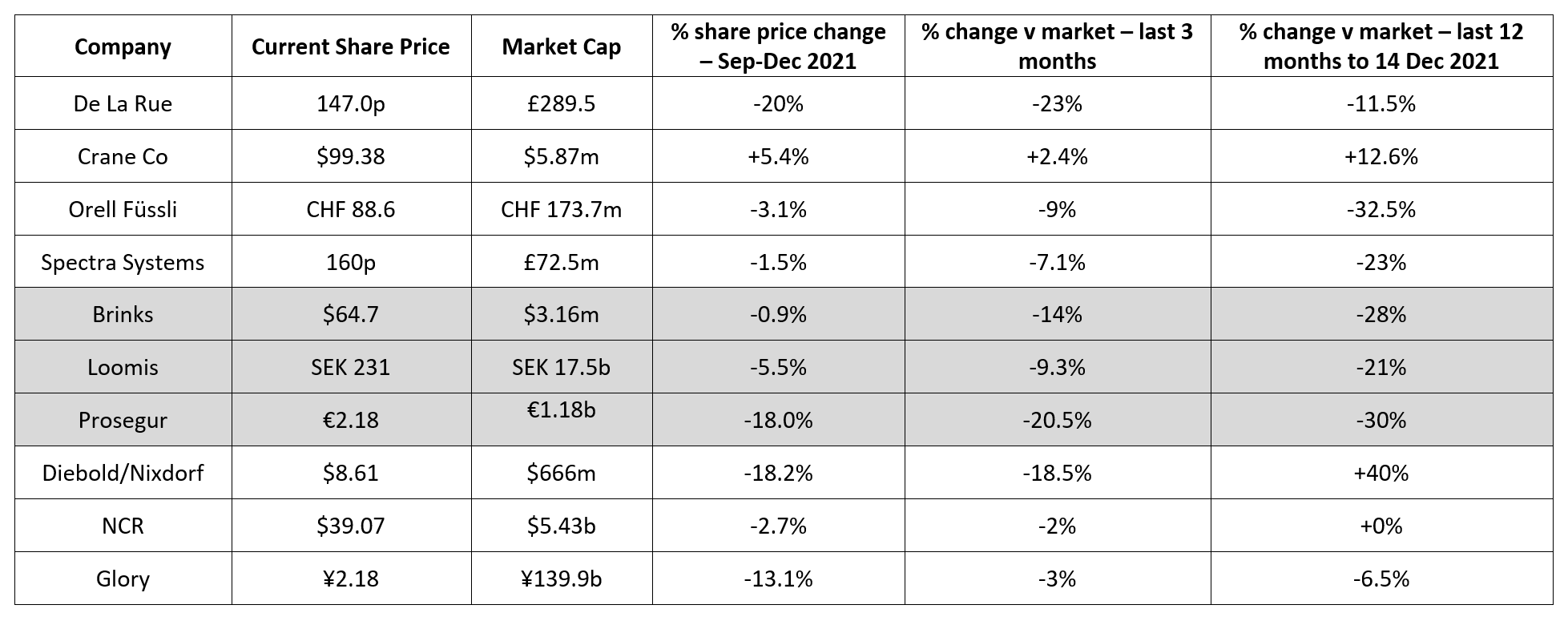

Our quoted companies’ share prices, with one exception, all declined in value in the period and underperformed their markets for the second quarter in a row.

In the 12-month period the picture is very similar – eight of our companies underperformed their markets, six by over 20%, one tied its market and one outperformed by 12.6%.

Substrates and banknotes – Crane Co the outlier

De La Rue’s share price has spent all this period below its value at the end of the last period. It had fallen by 10% on 4 October and remained mostly between -10% and -17% until 24 November, when the company announced its interim results, after which it fell to -26.5%. This was despite announcing an increase in revenue of 0.9% to £177.6 million and in adjusted operating profit of 13.7% to £13.8 million. The market was obviously expecting more!

The company’s share price has since recovered somewhat to -22%, underperforming its market both in this period and in 12 months.

Crane Co’s share price increased in the period by 5.4% to $99.38. Its share price never fell below its starting value of $94.25 and peaked at 17.5% above it in mid-November.

The company outperformed it market in the period by 2.4% and in the year by 12.6%.

Orell Füssli’s share price fell by 8.4% last period (July-September) as it announced a fall in both revenue (-6.5%) and operating profit (-4.6%). In this period (September-December) the Swiss stock market, the SMI, increased in value by 10.5% while Orell Füssli’s share price fell by 3% to CHF 88.6, giving it a market value of CHF 173.7 million.

Consequently, the company underperformed its market - in the period by 9.0% and in the year by 32.5%.

Spectra Systems Corp’s value fell slightly in the previous period to £73.5 million despite the company reporting a revenue increase of 23% and an adjusted operating profit increase of 44% to $3.52 million in the first half of 2021.

This period its share price fell slightly (-1.5%), leading it to underperform its market by 7.1% and in the full year by 23%.

CIT – market values decline despite resilience

Brinks Co is enjoying a good year despite COVID. Revenue was up by 11% in the third quarter and it reported EBITDA of $170 million, producing a 15.8% operating margin.

These results enabled it to forecast that its year end results would show a 12% increase in revenue to $4.1-$4.2 billion, and a 22% increase in operating profit to $460,000-$470,000. Its EBITDA increase is forecast at 17% to $655,000-$675,000, an operating margin of 15.9%.

Surprisingly, the share price did not gain in value, but fell slightly (- 0.9%). Given the market’s increase in value during the period, Brinks underperformed its market by 14% and in the year by 28%.

Loomis released its interim report, January-September 2021, on 3 November. Revenue for the nine months was slightly higher (+0.8%) at SEK 14.397 billion and operating income (EBITA) 0.5% higher at SEK 1.36 billion. It was able to report that during the second and third quarters this year, the overall impact on revenue and operating margin from the pandemic was lower compared with the corresponding period in 2020.

The report’s release caused an initial 10% surge in the share price, but this was short lived and by the end of the period, probably due to concerns about the possible impact of the Omicron variant, the share price had fallen by 7% to SEK 231.

In the period Loomis’ share price underperformed its market by 9.2%, and in the full year by 21%.

Prosegur also released its results for the first nine months in the period, but comparing the results for 2020 and 2021 is difficult due to the sale in 2020 of 50% of Presugur’s Spanish alarms business and other extraordinary items.

If these are excluded, sales in the first nine months of 2021 fell by 3.2% to €2.5 billion, profit (EBITA) by 9.6% to €159.4 million (margin 6.3%) and EBIT by 11.1% to €137.1 million (margin 5.4%).

In the period Prosegur’s share price fell by 18%. It underperformed its market by 20.5% and in the full year It underperformed by 30.0%.

ATM and service providers all decline in value

Diebold Nixdorf’s results for the first nine months of 2021 showed an improvement over the same period in 2020. Sales increased by 1.8% to $2.845 billion and operating profit by 380% to $87.8 million (margin 3.1% versus 0.7% in the first nine months of 2020). The net loss was reduced from $217.4 million to $40.4 million.

Despite this improvement, in the period its share price fell by 18.2%. It underperformed its market by 18.5% and in the year by 40%.

NCR also announced its results for the third quarter and first nine months in the period. Like Diebold Nixdorf, it had a good third quarter, with revenue 20% higher at $1.9 billion and operating income 33% higher at $157 million. For the nine-month period revenue was 12% up at $5.1 billion and operating profit (EBITDA) 39.6 % higher at $891 million, a margin of 17.4%.

Despite this improvement, NCR’s share price fell by 2.7% to $39.07, and it underperformed its market by 2%, but in the year, it matched its market’s performance.

Glory reported a much improved first half compared with H1 2020. Revenue in 2021 increased by 16.4% to ¥103 billion and operating income (EBITDA) by 54.7% to Yen 13.7 billion.

Despite this marked improvement over the same period in 2020, its share price decreased by 13.1%. It underperformed its market by 3% and in the period and 0.5% in the year.

Subscriber content

Read the full article

Full access to Currency News articles, newsletters and archives.