Cash Access in a Less-Cash World

In the November issue of Currency News™, we covered initiatives in Australia and the Netherlands to assess the growing trend to digital payments and what these countries are doing, or beginning to think about doing, to ensure ongoing access to cash in a less-cash world.

This month is the turn of France and Israel, representatives from the central banks of which both gave presentations at the recent Europe Cash Cycle seminar. This and the following article are summaries of those presentations.

Less cash is not a cashless society

According to Raymond de Pastor, from the Cash Department at the Banque de France (Bdf), in his presentation titled ‘Less Cash is not a Cashless Society’, cash use is declining in France. This is creating issues that need to be resolved quickly if cash is to remain as a means of payment available to all in the future The BdF, like the De Nederlandsche Bank (DNB), is carrying out its own review of the cash cycle in parallel with the ECB’s 10-year review. It is based on the premise that there will be less cash but not a cashless society.

In 2010 there were three main means of payment – cards, cash, and cheques. Since then, other forms of digital payments, in particular contactless card and mobile payments, have increased substantially, while cheques have almost disappeared.

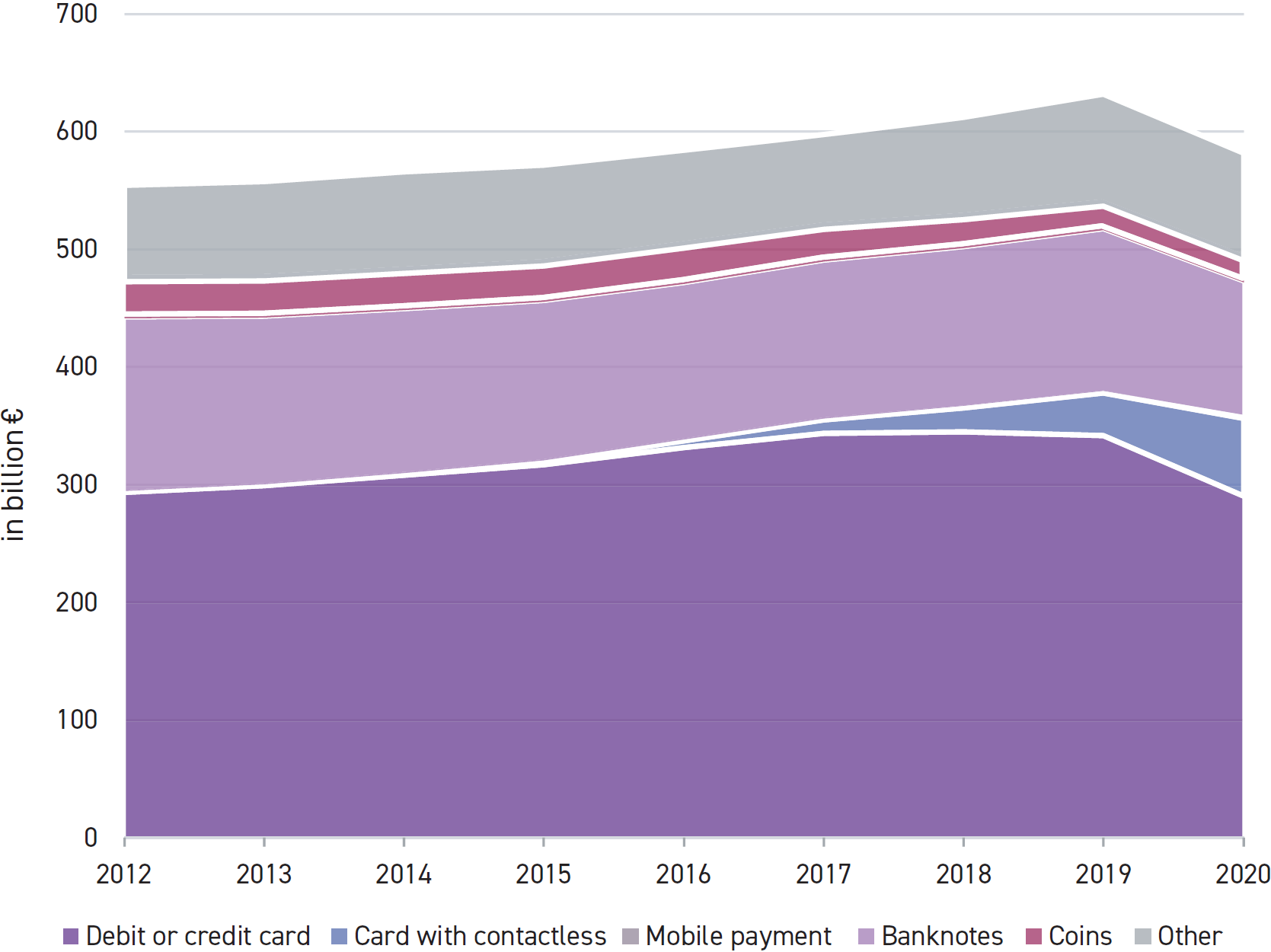

Between 2016 and 2019, cash used as a payment instrument declined by 10% in volume to approximately 58% of transactions, and by 4% in value to around 25%. In 2020, with the advent of COVID-19, the use of cash at POS declined along with all other payment methods, except for the use of cards with contactless payments, which increased substantially (see chart below).

Distribution of households consumption expenditures among means of payment (POS, value terms). Source: Banque de France.

Distribution of households consumption expenditures among means of payment (POS, value terms). Source: Banque de France.The BdF’s analysis of cash trends during the pandemic in 2020 showed a sharp decrease in lodgements due to an accelerating change in payments behaviour (more digital) and a drop in household spending. The ratio of card payments/ATM withdrawals showed sharp increases, leading to the conclusion that a substantial amount of cash was most likely being used as a store of value.

The background to reviewing and revising the National Cash Management Policy (NCMP) takes place as the flow of banknotes from the general public to professional cash handlers (credit institutions, CIT companies and the BDF) is declining, but the net demand for banknotes remains positive, reflecting the so called ‘paradox of cash’ – the use of banknotes for precautionary reasons and a buoyant international demand for the euro, leading to net issuance increasing by 650 billion banknotes (from 800 billion to 1,450 billion).

This phenomenon is not limited to France – similar growth trends have been recorded around the world. The conclusion is that a decline in cash usage for transactions does not necessarily mean the end of cash.

France’s NCMP guarantees citizens the freedom to choose their means of payment. But the decline in the use of cash for transactions is creating challenges for the cash cycle, such as how to maintain an organised and resilient system and how to provide a national network of cash distribution and collection points as the unit costs increase.

Managing the decline

The NCMP aims to address these issues by managing the decline in the use of cash in an orderly manner by involving all cash stakeholders. It has a high level steering group – The Cash Industry Steering Committee – which is chaired by the BdF and includes all the direct stakeholders in the French cash industry Of note is that France in 2015 adopted a National Cashless Payment Strategy, which it updated in 2019. It sets out the strategic guidelines and operational initiatives for the French financial sector and is based on the dual principle of neutrality and free choice of means of payment, not favouring one means of payment over another and not seeking to influence public behaviour.

The NCMP is designed to supplement this strategy with an equivalent holistic approach for cash.

The five challenges

Those involved in developing the action plan to create the NCMP identified five challenges and suggested responses.

1. The acceptability of cash as a means of payment. Cash is legal tender in France and is often the only means of payment available for the most vulnerable. Although to refuse cash in a transaction is a criminal offence, cases of refusal do occur and did so in the pandemic. Since the cost of managing cash for a merchant will increase as cash declines, more are likely to stop accepting cash as a payment.

In response, the BdF will officially remind the main retail federations and many retailers of cash’s legal tender status. Also, it will assess the legal and non-legal options to ensure that legal tender is respected. Another possibility is an annual survey of selected retailers or retail federations to monitor cases of refusal or discouragement.

2. Accessibility of cash. Although access to cash is currently satisfactory, there are differences between mountainous, rural, and urban areas and in the latter between city centres and outskirts. Where the profitability of ATMs is uncertain, alternative channels, eg. cash-in-shop, cash back etc. are already developing.

In response, the working group has identified certain indicators to monitor the number of cash access points nationwide.

3. The quality of banknotes in circulation. The BdF has the statutory task of ensuring the quality of banknotes in circulation. It carries out checks on stakeholders.

The response will be the implementation of the NCMP and, because recycling will increase, the BdF will increase physical checks on notes returned to circulation by third parties, and will carry out sample checks of banknotes processed by CIT companies’ cash centres or directly withdrawn from ATMs.

4. Robustness. The cash industry must be able to respond operationally to all types of crises.

The BDF has developed, in conjunction with the cash industry, a confidential plan detailing operational responses to every type of crisis and an ad hoc working group of stakeholders aiming to define a global and coherent policy.

5. The Efficiency of the Cash Industry. As cash usage and volumes decline, unit costs for processing banknotes and coins will increase. Adjustments will be required such as the optimisation of production capacities, especially new automated cash centres and resources (staff, convoys), the maintenance of a robust, wide territorial network and cost containment to safeguard banknote competitiveness. Also, the environmental footprint of cash (transport, waste handling, energy consumption) must be considered and lowered.

The plan is to further restructure the cash centre network. There were 2,010 cash centres in 1980, 73 in 2010 and 37 by 2020. A further 14 are set to be closed in the second half of 2022 based on the level of processing activity, the volumes of banknote inflows and the proximity of other cash centres, reducing the number operating to 23. The situation will be reviewed again at the end of 2022 given the current uncertainties caused by the pandemic.

The NCMP aims to provide cash for all three main uses, as a means of payment, a store of value and for use outside of France, the objective being a less cash, but not a cashless, society.

Subscriber content

Read the full article

Full access to Currency News articles, newsletters and archives.