The Role of Cash Cycle Analytics When Considering Banknote Durability

Banknote durability is an ongoing topic of interest for central banks. More durable banknotes have a reduced impact on the environment and save the central bank money because they need replacing less often. They also tend to look better in circulation for longer, which is frequently associated with lower processing costs; if a banknote is fit for circulation it will get re-issued into circulation instead of being sent back to the central bank for assessment and destruction.

When central banks want more durable banknotes they often focus on the banknote specification. Central banks will move to polymer or add varnish onto their paper banknotes. These approaches are well proven to increase banknote lifetimes. However there are also other factors that impact banknote lifetimes.

There are conscious decisions that central banks can make to trade off banknote lifetime with the quality of notes in circulation. Lowering the fitness standards will allow banknotes to last longer. However, assuming the notes are returned for sorting frequently enough to be removed from circulation at the end of their useful life, this comes at a cost and impacts the quality of the notes in circulation negatively. Sorting machine calibration can also play a role – a few central banks have anecdotes about a moment when a sorting machine destroyed perfectly good notes. Regular calibration and careful consideration of the settings required will ensure that banknotes that are fit for purpose get re-issued into circulation.

There are other cash cycle analytics factors that enable banknotes to last longer without impact the quality of notes in circulation. One factor is the number of notes in circulation – if you are carrying one note in your wallet you will use it for your next cash payment, whereas that note only has a 10% chance of being used if you have ten notes in your wallet. Notes that are used more often will wear out more quickly. Some countries have circulating banknotes with impressive banknote lifetimes and no obvious circulation quality issues due to a very high number of notes per head of population.

The other factor is the denominational structure of your banknote series. If your country has a $20 as the highest value denomination and a restaurant bill comes to $100, then it requires at least five banknotes to pay that bill (and more banknotes if the payee has mainly $10 notes in their wallet). In this scenario at least five banknotes are being handled, which comes with the risk that five banknotes are wearing out ever so slightly. If, in the same scenario your country has a $100 as the highest value denomination then only one banknote is needed.

Most economies have at least low levels of inflation, which means the highest value storage-of-wealth note will eventually become transactional. As this happens, there is merit in considering the introduction of a new high value note (and possibly also transitioning the very lowest value note to coin). The optimal denominational structure will reduce the number of banknotes that a central bank has to purchase and reduces the stress on the cash cycle (eg. the volume of notes needing to be stored may reduce, the frequency of ATM replacement may reduce).

In extreme scenarios of hyper-inflation the difference between regularly introducing new high value denominations or not can represent millions of dollars in banknote spend. Despite concerns by some central banks, analysis at De La Rue has never found a causational link beyond the banknote denomination structure and inflation. In inflationary situations, new high value notes simply help a country manage the situation they are in.

For economies experiencing lower levels of inflation, it is still prudent to consider the optimal denominational structure and the potential efficiency gains periodically. One empirical model that supports central bank discussions on this topic is De La Rue’s D-Metric™ model.

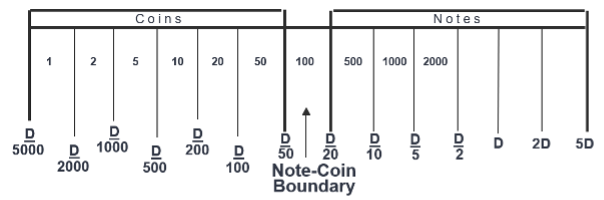

Research during the 1970s revealed that there was a remarkably robust empirical relationship between wages and currency. This led the D-Metric model, which is an empirical model that demonstrates a relationship between the daily average wage and the denominational structure of a country. De La Rue has used the D-Metric model over the past 40 years to demonstrate a relationship between the average daily wage and the denominational structure of a country. Today D-Metric analysis, combined with the cash cycle analytics platform DLR Analytics™, supports central banks making data-driven decisions about their cash cycles.

The D-Metric model is best explained with the diagram above. In this example, the banknote denominations have been assigned to the appropriate section of the diagram.

For instance, the 1000 is an amount of money that is somewhere between 1/10th and 1/5th of the average daily wage. The diagram is unusual in that the top three note slots are not occupied and would indicate that new higher value denominations should be seriously considered. Recent De La Rue analysis of 48 countries revealed that 42% of countries have a note in the top position (ie. between 2D and 5D) and 73% of countries have a note in the second highest position.

The model is conceptually very simple but requires some skill and careful mathematical modelling to ensure it is applied correctly. Accurate and representative daily wage information can be challenging to obtain yet essential for the model, and requires some specific checks before being applied. Variants of the model based on consumer price indices and other economic indicators have been demonstrated to work in certain situations when the daily wage information is not available (for fun, in 2017 we even demonstrated that the Big Mac Index published by The Economist newspaper had useful applications).

Overall, there is a suite of cash cycle analytics tools available to central banks and, although more durable substrates play a critical role in banknote lifetimes, there is merit in thinking about banknote durability more broadly than simply the specification of the note.

Subscriber content

Read the full article

Full access to Currency News articles, newsletters and archives.