How Ukraine is Managing Cash in a War

Whilst the Russian invasion of Ukraine exactly one year ago may have come as a surprise to many, it certainly didn’t to the Ukrainians themselves, who as early as Autumn 2021 were taking steps to minimise risks to the cash supply chain and decentralise the storage of cash stocks in anticipation of major disruption.

Over the course of the last 12 months, the National Bank of Ukraine (NBU) has maintained the supply of cash and cash circulation to over 1,500 bank branches and more than 3,800 ATMs across the country. The Deputy Governor, Oleksii Shaban, shared their experience, providing information about the impact on cash up until last September.

Cash is managed through the central vault, four cash circulation units of the NBU located in different regions of the country, and authorised commercial banks.

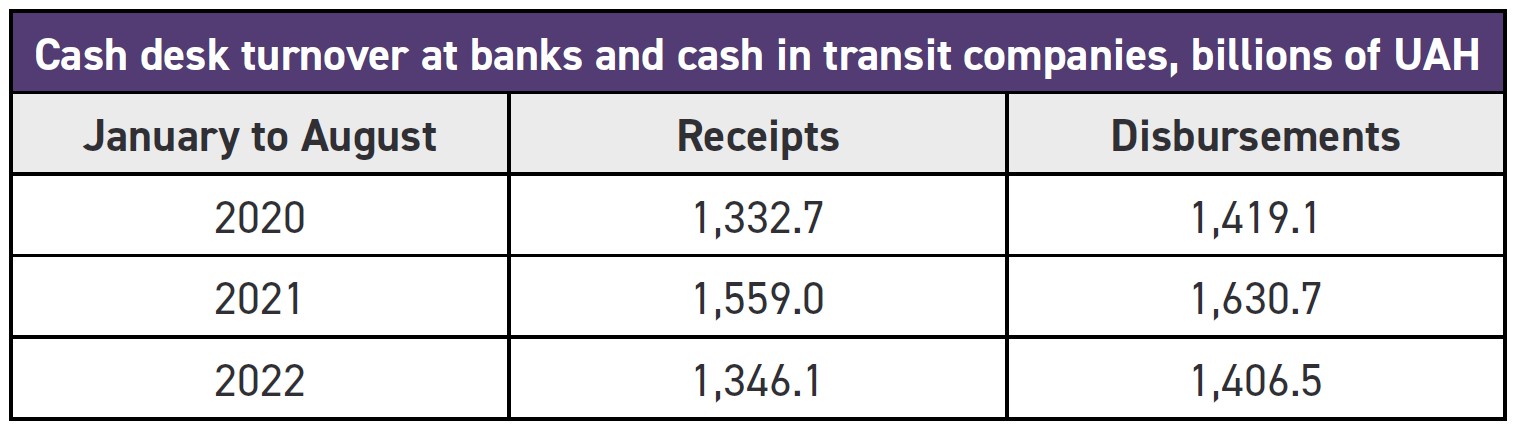

The Russians invaded at the end of February 2022, leading to a sharp increase in demand for cash. The annual growth rate of cash in circulation (CIC) was 19.9% in February 2022, CIC increased by UAH 51.2 billion in February. To give a sense of scale, in 2020 the peak monthly increase was in May, when it grew by UAH 28.5 billion. In 2021 the peak increase was UAH 31.4 billion in December.

This increased demand lasted through to mid-March when it peaked at 23.7%. It has decreased since then. From May 2022 there was a slow revival of activity in most sectors of the economy.

Shortly after Ukraine was invaded, the NBU fixed the hryvnia’s exchange rate and imposed capital controls. To prevent a run on the banks, the NBU announced it would provide unlimited hryvnia cash and loans to ensure banks could meet withdrawals needs.

Existing risks related to military action have led to a significant reduction of cash turnover at banks. War has caused major destruction, the occupation of parts of Ukraine, disruption of supply chains and a growth in cashless payments.

Actions taken to maintain cash circulation

Operations were only performed if there was no direct threat to the life and health of staff and clients of banks

Cash was allowed without limit

Cash handling requirements were relaxed:

No limits on ATM refills

No cap on cash stored in vaults

Purchase with cashback was recommended to merchants

Banks were allowed to receive cash free of charge for pay outs to those serving in the Armed Forces. Banks were required to transfer cashless funds from the bank’s correspondent accounts and state the intended use of the cash.

A daily limit of UAH 100,000 was set for hryvnia cash withdrawals from client accounts in Ukraine.

In order to safeguard cash stocks, some stocks were moved from Kyiv to the western region, daily monitoring of cash stocks at authorised banks was strengthened, stocks in regions with military action were reduced and banks in occupied territories were authorised to make their stocks unfit for issue using mechanical means.

Due to the destruction and disruption of the road network, much of the movement of cash was switched to the rail network. Before the war, Ukraine had over 2,000 armoured cash in transit vehicles. In the first four months of the war, 43% were handed over to the military. In addition, many of the staff at CIT and cash collection units were mobilised.

The cumulative effect has been to make cash collection and transportation harder. As a result, cashless payments have become more important. At the start of the war, 72% of people over the age of 15 had payment cards and 62% had mobile phones. Ukraine’s digital payment systems have continued to work both nationally and internationally, and the central settlement system has also worked. The NBU has been encouraging citizens to use digital payments where they can, and to access cash from shops rather than from ATMs or bank branches where possible.

Arrangements for cash processing

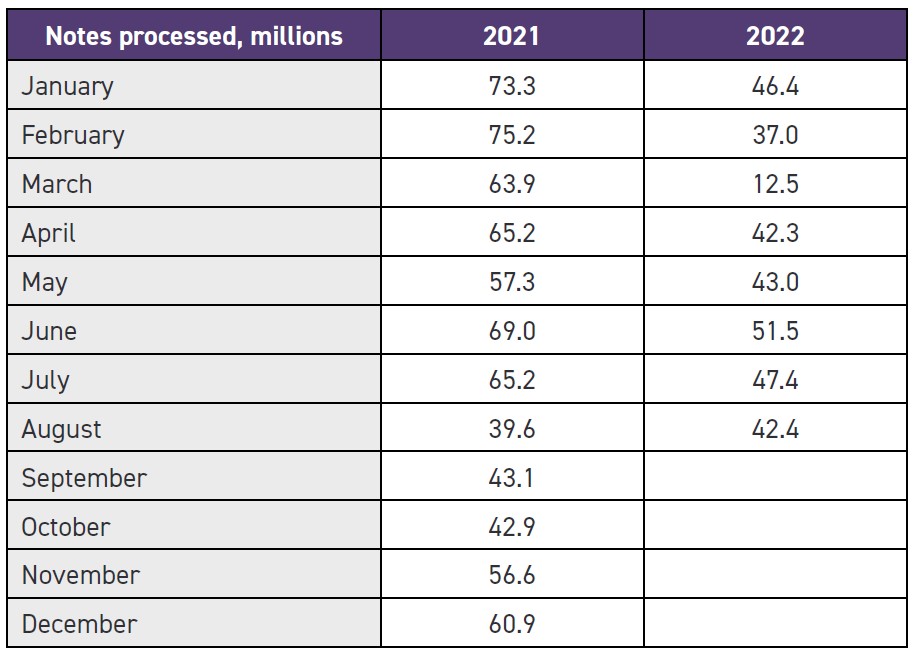

The NBU uses 9 BPS M7 and 13 BPS 1040 sorters to process cash. Staff reductions due to mobilisation and air raid warnings have disrupted cash processing. As a result, cash processing volumes have been reduced.

One response has been the temporary suspension of fitness and authentication requirements for banks and CIT companies authorised to process cash, allowing them to dispense unfit notes provided they still comply with regulations on authenticity.

Cash management outside of Ukraine

In the first months after the Russian invasion, Ukrainian refugees in the EU faced exorbitant commissions when attempting to exchange their funds for local cash. The Council of the European Union recommended that EU member states allow refugees to convert up to UAH 10,000 hryvnias without charge at the NBU’s official exchange rate.

Moreover, the NBU signed agreements with nine central banks of other European countries to purchase hryvnia from refugees who had fled to their countries. These agreements ran from March through to December. Between 28 March and 16 September 2022, UAH 935 billion was exchanged for euros, broken down by Poland (728), Germany (144.8), Netherlands (26.1), Switzerland (12.4), Belgium (9.1), Italy (8.9), Sweden (5), Latvia (0.7) and Malta (0.1) NBU also entered into agreements with three commercial banks in Austria, Hungary and Moldova, which between them purchased UAH 1.24 billion from Ukrainian citizens abroad and returned this to Ukraine between 15 April and 7 September.

At the recent World Banknote Summit in Antwerp, Barbara Jaroszek of Narodowy Bank Polski (NBP) gave a presentation on the scheme (the NBP was the first to sign an exchange agreement with the NBU) and how it worked in Poland (the largest recipient of Ukrainian refugees and largest supporter of the war effort in Ukraine).

Poland has a population of 38 million, and Ukraine 44 million. 9.27 million refugees have crossed the 535 km border into Poland, of which 7.44 million have either returned or moved on elsewhere. 1.5 million Ukrainians are still in Poland.

At the outset of the war, and the sudden influx of refugees, daily cash withdrawals were x17 the daily average in 2021. In eight days, the equivalent of the whole of the first quarter of 2021 cash withdrawals were withdrawn in Poland.

The exchange rate fell x10 in one day. As a result, NBU moved to guarantee the exchange rate. The formal exchange agreement came into effect 30 days after the war started. NBP had to find commercial partners for cash distribution, and to organise processes for the repurchase, sorting, authentication, checking and storage of Ukrainian currency. Staff training in dealing with a foreign currency was required, and legal and procedural risk has to be managed. A key priority was to stabilise the exchange rate.

A total exchange rate limit per person of UAH 10,000 (c €290) was set. The initial agreement was for three months but extended to September. Only UAH 100, 200, 500 and 1,000 denominations were accepted (NB. Ukraine has ten denominations and two series in circulation). The exchange rate was communicated weekly by NBU to NBP, but in the end there have only been small variations. No exchange fees were charged.

The agreement limited exchanges to a total of UAH 10 billion. But this proved to be significantly more than was required, as the actual value of purchased notes was UAH 72.8 million, 7% of the total sum agreed. The number of transactions was over 100,000 and the average value was UAH 7,084. The amount exchanged in Poland was much more than any other European national central bank.

NBP also served as a logistical hub for storage and future transfers back to Ukraine for the other European countries with similar exchange agreements.

According to Barbara Jaroszek, the operation ran smoothly. There were no legal or technical problems, neither were any counterfeits or heavily damaged notes found.

The exchange agreement serves as a model for future use, she said, concluding that the decision to support Ukraine in this way was about restoring their sense of independence and dignity by showing that their currency still counted.

Power banking to overcome blackouts

By late Autumn, Russia turned its attention to knocking out Ukraine’s power grid and energy infrastructure, with widespread blackouts throughout the country. To counter this, the NBU set up the POWER BANKING initiative – a joint banking network involving all 14 systemically important banks in Ukraine – to provide banking services to clients even during blackouts. The 1,000 branches of these banks and other banking providers that make up the joint network all have alternative energy sources, backup communication channels, enhanced cash collection capabilities, and additional staff.

As of the time of writing, over 2,300 branches have joined the network, representing 70% of all bank branches in the country (excluding the closed ones and those located in the occupied areas and in and around the battle zone). The NBU provides a map on its website showing which banks are participants and where banking services, including cash withdrawals, can take place.

Final word

The impact of the war is starkly shown in this data and report. Pragmatism, flexibility and ingenuity have been necessary to allow the Ukrainian cash cycle to continue functioning and, hopefully, to recover.

Subscriber content

Read the full article

Full access to Currency News articles, newsletters and archives.